Picture supply: Getty Photos

I imagine investing in FTSE 100 shares is a wonderful solution to construct long-term wealth. It’s why I proceed prioritising blue-chip shares from the Footsie index (together with a smattering of high FTSE 250 shares).

Investing in shares generally is a wild journey when information movement adjustments and investor confidence sinks. However over the long run it may present life-changing wealth in retirement.

And following recent analysis on how a lot cash I might have as soon as I end work, my technique of investing any further money I’ve has taken on better significance.

£738k pension pot

As I’ve beforehand reported, the Pensions and Lifetime Financial savings Affiliation (PLSA) final week upgraded its forecasts for a way a lot the common single Brit might want to retire comfortably. Its newest estimates will be seen under:

| Way of life | Former forecast | New forecast | YOY change |

|---|---|---|---|

| Minimal | £12,800 | £14,400 | + £1,600 |

| Reasonable | £23,300 | £31,300 | + £8,000 |

| Comfy | £37,300 | £43,100 | + £5,800 |

To not be outdone, monetary companies supplier Quilter additionally raised its estimates on the scale of the pension pot the common single particular person will want for a snug life-style in retirement.

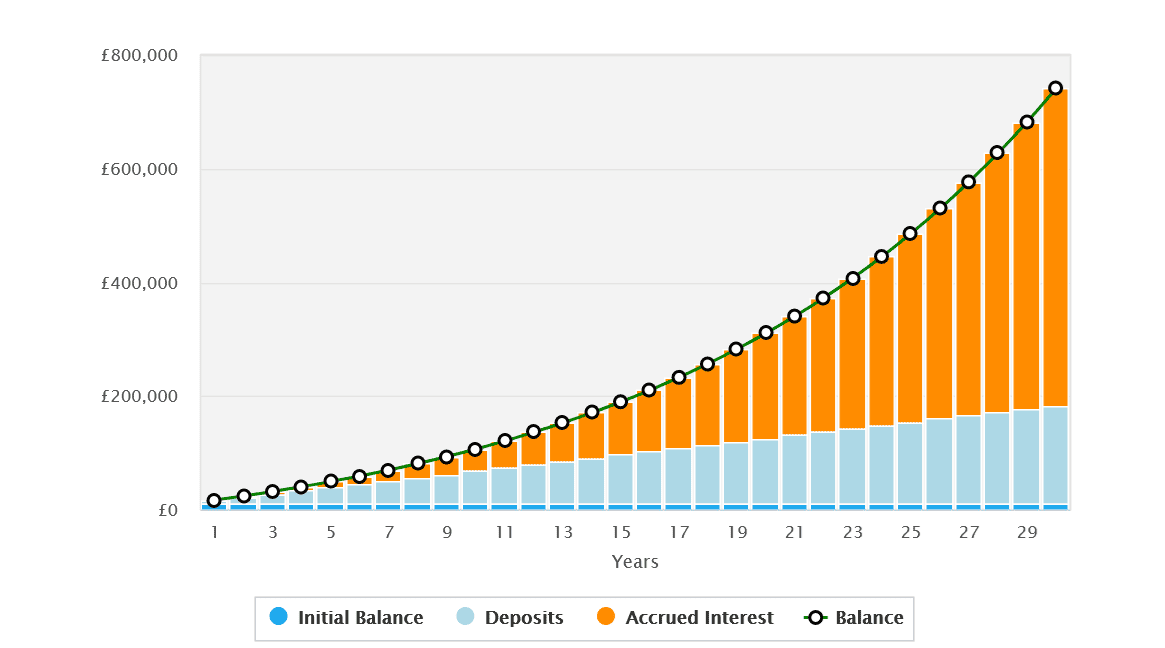

The brand new determine stands at an eye-popping £738,000. That’s up a whopping £100,000 from Quilter’s earlier forecasts.

Jon Greer, head of retirement at Quilter, mentioned that the PLSA’s newest forecasts present that it “will take a concerted effort to realize a pension pot required to fulfill the distinction between the [required income level] and that supplied from the complete State Pension“.

Hitting the goal

The precise quantity wanted to retire differs from particular person to particular person. However that analysis gives a helpful information for all of us. And it clearly makes for sobering studying.

Nevertheless, I’m not letting panic take over. By beginning my funding journey early and frequently shopping for FTSE 100 shares, I’ve an excellent probability of hitting that focus on laid down by Quilter.

The UK’s premier share index has delivered a mean annual return of seven.5% since 1984. If this development continues, after 30 years I might — with an preliminary funding of £10,000 and an everyday month-to-month funding of £480 — create that pension pot that Quilter recognized.

A high FTSE 100 inventory

Previous efficiency isn’t a dependable information of what I can anticipate. However the Footsie‘s wonderful long-term returns present what I might probably obtain over the long run.

And by constructing my portfolio round sturdy, multinational corporations with robust stability sheets, I can enhance my possibilities of hitting my retirement objectives. We’re speaking about companies like Reckitt (LSE:RKT), which owns main shopper healthcare manufacturers like Strepsils lozenges and Durex condoms.

Regardless of the issue of rising prices, this Footsie share nonetheless has an distinctive document of rising earnings with its standard labels. And it has appreciable monetary clout that it may use for advertising and marketing and product innovation to maintain gross sales rising.

Reckitt additionally has important publicity to fast-growing rising markets that it may leverage to generate long-term earnings progress. By surrounding these types of shares in my portfolio with some high-risk, high-reward FTSE shares, I believe I’ve an important probability of having fun with attaining a snug life-style once I retire.